The concept of the Trans-America Grid (TAG) involves locating new power plants at the coal reserves (near the mine mouth) and then transmitting electricity, in bulk amounts, to distant customers via new and existing EHV AC and high voltage direct current (HVDC) transmission lines. This allows coal to be used for energy without the high cost of transporting the coal via rail to power plants that are traditionally located near the customer. This is literally transporting coal by wire.

The construction of new transmission lines and utilizing existing transmission lines allows the project to take advantage of weather and time zone changes between market regions to enhance the value of the coal-fueled generation. This ability to enhance the value of generation has not previously been available because of the isolation between the east and west grids of the United States.

TAG will integrate with the existing bulk transmission system to enable power to be transmitted from coast to coast. In addition to the obvious time zone differences to enhance the value of the coal fueled generation, weather differences (as fronts generally move from west to east) will provide a significant enhancement of value by allowing more base load energy to be sold at peak times. The advent of deregulation in the United States offers the project the opportunity for increased profit margins from both the sales and cost sides. From the sales side, deregulation offers the opportunity for higher prices on peak.

On the cost side, the project's ability to provide greater amounts of energy into market regions during times of peak at base load costs further increases margin. With variable operating costs as low as $4/MWh, the project will not only provide higher margins, it will also be the low cost producer ensuring revenue throughout the project's long life.

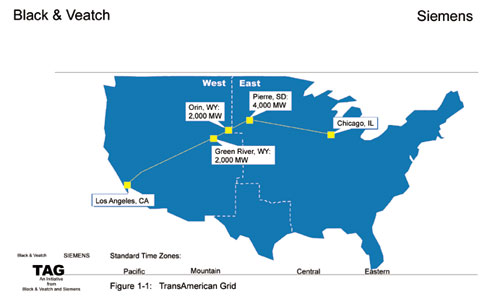

The project will be implemented by building 8,000 MW (nominal) of generating capacity with 2,000 MW coal plants, each consisting of four standardized 500 MW units, located at sites in Pierre, South Dakota (two plants); Orin, Wyoming; and Green River, Wyoming. The plants are located at sites that provide the lowest possible fuel costs consistent with cooling water availability and permitting requirements. EHV AC and HVDC transmission lines will be constructed along existing right-of-way to markets in the west and upper Midwest which in turn connects to the rest of the eastern grid. The plants will be interconnected, allowing the low cost energy to be sent either east or west to obtain the highest margins. The modular aspect of the project provides unlimited flexibility with respect to staged implementation. Commercial operation of the first unit is scheduled for 2005. The complete system is expected to be operating in ten years.

EAST-WEST BRIDGE TO BE BUILT

One of the most exciting aspects of TAG is the construction of the HVDC facilities interconnecting the east and the west grids. The lack of this transfer capability has historically stymied western coal mine mouth projects in the past. The magnitude of this project makes the east-west transmission interconnection feasible. The proposed HVDC transmission lines are shown in Figure 1-1. Current east-west transfer capability is approximately 1,000 MW, which is virtually all subscribed. Through the HVDC transmission lines, TAG will add 6,000 MW of capability that can be provided to either the east or west grids as physical assets in each marketing region. The HVDC transmission lines to marketing regions in the west and upper Midwest allow access from the coal-fueled units in the Powder River Basin that is not available from the existing grid. The HVDC transmission line to the upper Midwest connects with the existing 765 kV transmission system, allowing access all the way to the east coast.

UTILIZATION OF MOST PLENTIFUL/LEAST EXPENSIVE COAL IN US

The coal supply for the proposed power generation plants will be from mines located within the Southern Powder River Basin (SPRB) of Campbell and Converse Counties, Wyoming. The coal reserves of the SPRB constitute the bulk of the economically mineable reserves of the larger Powder River Basin (PRB).

The total reserves of the overall PRB are enormous, constituting the coal equivalent for the United States of world oil reserves to the Middle East. The total reserve base is conservatively estimated to be in excess of 141 billion tons, of which about 58 billion tons are projected as being readily and economically capable of extraction by present-day surface-mining technologies. The 58 billion tons represents over 50 years of the total United States coal consumption compared to only 9 years of natural gas reserves for North America.

The coals of the SPRB are subbituminous in rank, ranging in heating value (as-received basis) from about 7,500 to 9,000 Btu/lb, with the bulk of the current production ranging between 8,200 and 8,900 Btu/lb. Sulfur content is low (range of 0.1 to 1.7 percent, with typical values of 0.4 to 0.8 percent), and thus the coals are well suited as compliance coals under the US Clean Air Act (1990).

As a result of the highly favorable mining conditions of the SPRB, extraction costs are the lowest of any mining region within the United States. These low production costs, coupled with large-scale mining operations under competitive market conditions and highly developed rail infrastructures (both existing and proposed), enable the SPRB coals to aggressively compete against coals from other sourcing regions throughout most of the United States.

The siting of the power plants makes them relatively proximate to the SPRB mines, thereby minimizing rail haulage distances. This maximizes the opportunity for TAG. The additional benefit of using PRB coal is the stability of supply. The SPRB mines, both existing and projected, have the reserves capability to supply the coal supply requirements of the United States for at least 40 years into the future. As a result, the stability of the pricing of coals, compared to alternative fossil fuels such as natural gas, is assured.

DELIVERY OF POWER TO VIABLE MARKETS

The generated electricity would be transported by new HVDC transmission lines to the following primary destination markets as indicated on Figure 1-1:

* Chicago area and

Upper North Central US (Northern Illinois, Northern Indiana, Wisconsin,

and Minnesota).

* Southern California (Los Angeles and vicinity metro areas).

* Secondary destination markets for which transmission corridors could

be developed at a later date as extensions of the primary

grid would include the following:

* Northern California (San Francisco Bay and Sacramento metro areas).

* Northern Utah (Ogden-Salt Lake City metro area).

* Southern Nevada (Las Vegas-Clark County) and Central Arizona (Phoenix-Tucson

metro areas).

* Colorado (Boulder-Denver metro areas).

* Central Minnesota (Minneapolis-St. Paul metro area).

* Northern Texas (Dallas-Fort Worth metro area).

PROJECT SCHEDULE

A staged schedule is currently anticipated, beginning with partial blocks of delivered power and single point-to-point connections. Initial construction would include 2,000 MW of coal-fueled generation and one HVDC converter station at Pierre, North Dakota, and a 2, 000 to 3,000 MW HVDC line to Chicago. Initial commercial operation is scheduled for 2005. The complete system is expected to be in operation about 10 years after the start of the project.

FINANCIAL PROJECTIONS

The conceptual design and cost estimates are generally conservative at this point in the project. For example, the HVDC transmission lines included in the capital cost have an additional 4,000 MW of transfer capacity for which the economic benefits have not been included.

Total capital costs for both Phase I and Phase II will include plant construction costs, transmission construction, financing charges, and indirect construction cost. Stated in (1999) dollars, the total projected capital cost for the TAG project is approximately $15 billion.

Figure 1.1--The proposed HVDC transmission lines are shown at right. Current east-west transfer capability is approximately 1,000 MW, which is virtually all subscribed.